Oil posted a gain in July, boosted by a steadily weakening dollar and OPEC’s restraint on production.

Deep crude output curbs by the Organization of Petroleum Exporting Countries and its allies have helped futures rebound from their plunge below zero in April, yet the unprecedented cuts are set to ease in a matter of days. Still, U.S. crude inventories have showed signs of shrinking and are currently sitting at the lowest since April. The Bloomberg Dollar Spot Index is also set for its worst monthly performance since January 2018, bolstering the appeal of commodities traded in the U.S. currency.

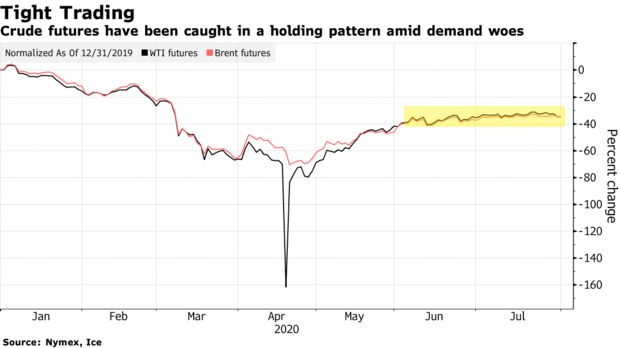

Yet, futures have remained trapped in a tight trading range with rallies limited by the coronavirus pandemic ravaging demand. Exxon Mobil Corp. said it only sees an oil consumption recovery well into 2021.

Adding to troubling signs over an economic recovery, U.S. consumer sentiment extended its slide in late July as the virus led to renewed business closings and layoffs. Exxon and Chevron Corp. posted the worst losses in a generation as the virus combined with a global crude glut battered their businesses.

Meanwhile, U.S. shale producers are also signaling supply will come roaring back over the next few months with futures near $40 a barrel. ConocoPhillips said this week that it will restart most wells that were shut by September.

“The big worry is that we’re about to go into August and this is the last two weeks or so of potential driving vacations,” said Bill O’Grady, executive vice president at Confluence Investment Management in St. Louis. “You’ve had depressed demand for gasoline and it’s probably not going to get a whole lot better from here.”

| PRICES |

|---|

|

OPEC+ plans to return about 1.5 million barrels a day to the market next month after cutting global supply by roughly 10% when demand plunged.

Pointing to further weakness, gasoline refining margins are at the lowest seasonal level in years, showing refiner profitability is facing pressure as the pandemic keeps Americans at home and off the road.

Whether or not demand will improve in the fall will depend on how much the resurgence of Covid-19 impacts commutes to work and children returning to school, with driving to and from school accounting for about 5% of gasoline demand, Phillips 66 estimated

Is this article helpful to you?

Share it now with your partners or friends

Không thể sao chép